Predetermination of benefits for dental insurance is a valuable resource when it comes to presenting treatment plans and discussing finances with patients.

You recommend an implant for a patient to replace their one missing tooth, and the first thing patient asks you is “how much will my insurance cover“, or “what’s my out of pocket cost“?

Your front desk has already verified their benefits with their insurance, and there’s an estimated 60% coverage on implant placement. So you tell the patient, “your out of pocket is going to be $x considering your insurance is expected to pay 60% towards this procedure.“

Patient accepts treatment. You do the implant and you send in a claim and it comes back DENIED. The response from the insurance is that the tooth was extracted when the patient did not have this insurance, so they will not provide benefit to restore the tooth in the area – this is what’s called a missing tooth clause.

Or worse, the consulting dentist at the insurance company decides to downgrade the implant benefit to a removable partial denture because they believe it’s the best course of treatment for the patient.

Now your office sends the patient a big bill at home notifying them that they’re responsible due to insurance non-payment. Patient is angry because he or she was told there was going to be 60% coverage.

Sound familiar? maybe not for implant placement, but for something else you expected payment for from the insurance – even AFTER verifying the patient benefits?

All of this can be avoided by sending in a Predetermination claim to get pre-treatment estimate benefit for a dental procedure.

In this post, I’ll cover:

- What predetermination benefit or pre-treatment estimate is

- Why you need it

- X-rays and adequate documentation you need for getting accurate estimates on TIME

- How I approach predeterminations in my office

Let’s dive right in.

Predetermination of benefits for Dental Insurance: What is it?

It’s a statement from the insurance company stating what they’ll pay towards the procedures you sent in on the Predetermination claim.

The statement will indicate if there are any downgrades to an alternative treatment option (implant vs a partial, PFM crown to a full cast metal crown only), any deductible that may need to be paid, what the insurance payment is going to be, and what the patient out of pocket responsibility will be.

Of course, at the bottom of the letter, it will also state that the “estimate is subjective to their plan and how much they have remaining on the plan once the treatment is completed.” What they’re saying is, the Predetermination statement is NOT a guarantee of payment.

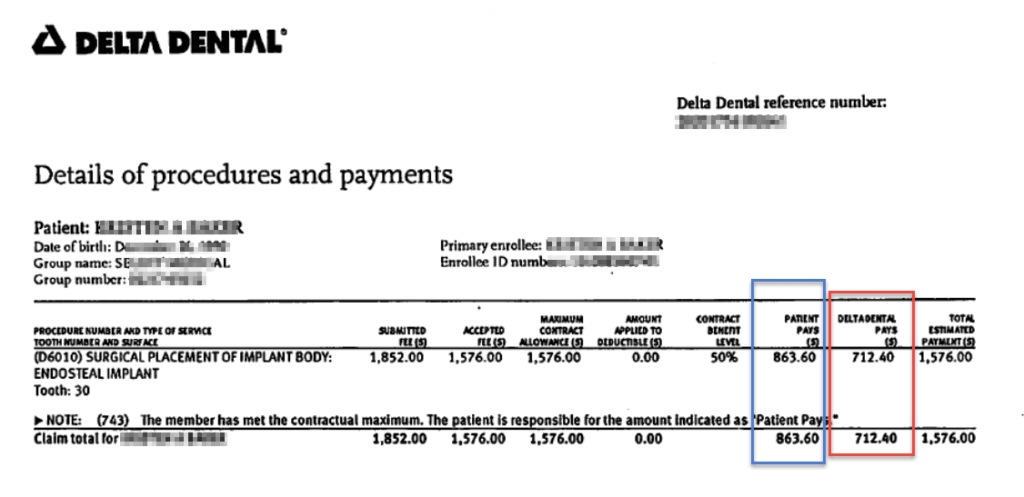

Here’s a predetermination for my patient that my office sent out for getting pre-approval for patient’s implant work:

When you receive the statement in mail, it will indicate the date as of when this was processed by the insurance company.

So as of that date, the insurance determines what they’ll pay towards the procedures depending on what the patient has left to use out of their yearly maximum.

So according to the picture, it states they’ll pay $712.40 towards the implant placement.

However, the patient came in and got some other work done after this Preauthorization was sent out and processed, so she ended up using some of the insurance money out of the maximum – which is not reflected in the statement you see above.

So even though the letter states they’ll pay $712.40, on the of the date of implant placement, since she only had $600 remaining on her plan, that’s the max the insurance will pay instead of the quoted $712.40 on the Predetermination statement.

This is exactly what the insurance means when they say “approval does not mean GUARANTEE of payment”.

Which means, patient pays a bit more out of pocket than what’s quoted on the statement.

The patient also received a copy of this at home, so they will ask you when checking out, so always keep the predetermination handy – when you’re collecting copays.

You not only need to look at what’s quoted on the statement, you also need to make sure of how much of the yearly maximum the patient has used up already.

Depending on what practice management system you’re using in your practice, this information should be available by going to their insurance benefits section, which is pretty easy to obtain in Open Dental (the software I use in my practice).

Why do you need Pre-treatment Estimates?

When recommending treatment to patients who have dental insurance, they’ll want to know what their out of pocket cost is going to be. Patients want to find out an estimate of what the insurance will cover.

Most insurances will recommend a pre-determination to be done for procedures over $300. There are some plans that absolutely REQUIRE it for some procedures.

For example, in my office, I take some union plans (reasonably well paying ones), which REQUIRE us to send in a predetermination prior to moving forward with a crown. Otherwise, a payment is not guaranteed.

I don’t risk it, therefore, if a patient with that plan comes in and if the patient needs a crown, a predetermination with pre-operative periapical x-ray of the tooth is sent to the insurance.

From patients point of view, they want to know what their insurance will cover, so they can make a decision on how to move forward with the treatment.

From the office perspective, I want to know as the provider whether or not there will be coverage, so I can tell the patient: “Out of total cost of $x for this bridge, your insurance is expected to pay approximately $y dollars, and you’re responsible for the difference ($x-y).”

I do this to avoid SURPRISES. Financial surprises are usually the major headaches in most dental offices, and which I absolutely try to avoid. For services such as bridge, or bone-grafting / implant placement, dentures – I want to make sure there will be some coverage.

My front desk has already gone through the insurance verification process using our dental insurance verification template and we have a fax breakdown that shows there is x% coverage towards a bridge and implant services.

But I’ve gotten into a habit of ALWAYS sending a preauthorization for these services, so we can avoid telling the patient “well, your insurance didn’t end up covering your implant, so you have a balance of $x.”

For larger services, the left over balance resulting from insurance non-payment is usually large – and I can guarantee you the patient will be upset – even though you filed the paperwork for them and you verified their benefits for them.

At that point, they’re not going to value the time you and your team put in to educate the patient and doing all the paperwork.

This usually results in patient being upset and not being able to pay afterwards. You’ll hear something along the lines of “you can bill me” or “send me a statement”. Once this happens, it’s an uphill battle trying to collect from this patient, and you feel like you’re chasing the patient for money.

X-rays and Documentation for getting Predetermination of benefits:

Note: The information in the right column of the table below is everything I make sure to have PRIOR to starting the procedure. Not all plans require Predetermination to be done, but for the ones that do for any specific procedure, I’ve followed a routine to have all the information during treatment planning visit.

| Procedure | Recommended X-rays and Documentation |

|---|---|

| Root Canal |

|

| Crown |

|

| Bridge |

|

| Inlay / Onlay |

|

| Core-buildup (D2950) |

|

| Implant |

|

| Partial / Complete Dentures |

|

| Scaling & Root Planing |

|

What to keep in mind when offering Pre-treatment estimate to patients:

- Patients delay treatment: At my previous associateships, consultants that were hired often recommended to NOT send predeterminations because it only delays treatment.

Patient are less likely to move forward with treatment if we have to wait to hear back from insurance – which sometimes takes 3-4 weeks. I’ve had some insurances delay it even further.

However, there are patients that will ALWAYS want to know what they’re going to be responsible for before moving forward with treatment – especially if they’re not in pain. Of course I recommend they get started ASAP to avoid further problems and expense.

I usually tell them the maximum they’ll pay out of pocket (if there’s no coverage) will be the in-network fee (the maximum allowable) according to the insurance fee schedule. After completing the treatment, it’ll be sent to insurance and if they pay, it’s an additional benefit to them.

Some patients move forward with treatment, some don’t.

- Treatment denied deemed “unnecessary”: When insurance benefit comes back as denied, there are patients who will perceive it as “unnecessary”. No matter how much time you spent educating the patient, explaining the risks of delaying treatment – they are not going to move forward.

At this point – we explain to the patient that the last thing the insurance cares about is your well-being. It’s a numbers game to them – they have to payout less than what they receive in premiums – and there’s an upward trend with premiums going up with less and less coverage with more exclusions.

- Approval does not mean GUARANTEE of payment: This is always written on the Pre-determination benefit letter you receive back from the insurance.

What it means is that if a service in question is approved, it is still subject to other limitations and terms of the plan when submitting actual claim to the insurance after completing treatment.

For example: if a Predetermination for implant placement comes back as approved with 60% coverage and $800 of estimated insurance coverage – it means as long as the patient has $800 left in their plan at time you submit the claim after placing the implant – the benefit will be paid at the rate listed in the pre-estimate. If patient only has $300 left for the benefit year, the claim payment will only be for $300 and patient is responsible for the rest ($800-$300) – this is what I discussed above in the example picture of the Predetermination benefit statement.

I’ll get into this in detail in a future post when I go over how to READ the predetermination benefit response from the insurance.

How I approach Dental Predeterminations in my office:

Although most insurances recommend a pre-d for $300 and up, we only send it IF insurance absolutely requires it. Most will tell you that it is “recommended” but not required. I send it for implants, bridge and dentures only.

After getting burned by Guardian and Aetna for full mouth SRPs for nonpayment, I’ve started to send out preauthorizations for SRPs for patients with these two plans.

I try to follow couple of basic “rules” in terms of payments and financial policies:

1) We don’t send statements unless we ABSOLUTELY have to – Most bills never get paid. And if they do, it’s usually on a second, or third try.

2) For larger services: Bridge, Implants / Bone grafting, Partials and Complete Dentures – I always send a pre-d to receive pretreatment estimates even though we know there is some coverage towards those services. I want to make sure my team did not miss some “exclusion”.

When they’re verifying benefits over the phone and if the insurance flat out says there’s no implant benefits – then obviously we will not send a preauthorization for it.

3) BEFORE any service is rendered, financial arrangements are in place and PATIENT is aware of it

Conclusion:

I hope after reading the above you understand the basics of predeterminations or pre-treatment estimates.

If you haven’t downloaded the chart yet, click below to access it now. It’s a must have resource that you can print out and give to your front desk or personnel responsible for dealing with insurance in your office.

I have discussed how predeterminations are done in my office. So far, I’ve had no problems and patients are glad to find out their benefits PRIOR to starting treatment.

Although I do not want to let insurance dictate treatment, I advise all patients with same information, whether or not they have insurance, so they can make an informed decision to move forward. Some choose to move forward, some don’t.

In today’s economy, cost is the #1 factor why people avoid the dentist. According to a research article published by the American Dental Association Health Policy Institute in 2014, 40.2% of adults surveyed indicated that they will forgo dental care due to cost.

Give your patients different treatment options, phase delivery of treatment according to THEIR schedule, and present payment options that work for them. Do this for every patient – whether or not they have insurance, and continue moving forward to creating efficient systems in office when dealing with insurance.

If there’s anything you’re doing different that you’ve had success with, please don’t forget to leave in comments below and share with others.

Continue to tune in for our next post where I’ll continue on this topic of Predeterminations – Best Practices! – where I’ll show you how to put together quick templates that your team can use to attach to insurance claims!